Financial freedom: allowing you to spend your money and time on others

Five Cents Ten Cents has moved to http://fivecentstencents.com

Please update your bookmarks and new feeds are available at my new website!

============================

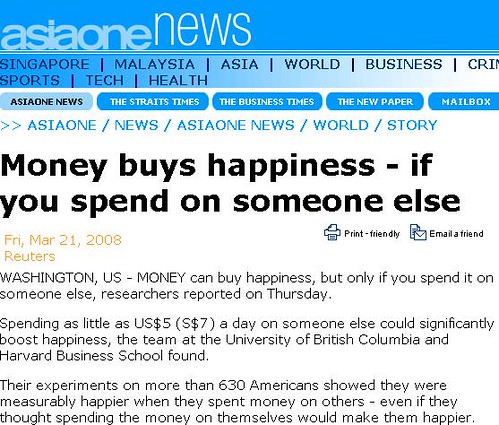

This article above has interesting implications from a financial freedom point of view. As you are on this journey towards financial freedom, do you consider the reason behind why you are driven towards this goal?

All human endeavour that seeks to achieve a certain degree of success requires effort, focus and perseverance. This comes only when you have a strong desire and a clear purpose as to WHY you are pursuing your goal.

Financial freedom is a worth-while pursuit when...

Financial freedom for the sake of financial freedom doesn't satisfy. I have alluded to this concept that you are drawn to achieve financial freedom because you want to escape the time-money trade-off or in simple terms the "rat race". The rat race sees us in this value-chain of getting up, going to work and fulfilling our role in the work-earn-spend-work cycle. Never ending when we are in thrall to our housing loans or other consumer debt.

To break free of this rat race is to be able to wake up and decide what you want to do with your time, energy and life without worrying too much about how you can feed yourself and your family. That, to me, is the practical dream that drives me towards financial freedom. It is the ability to make choices ordinarily not available to those who do not chose to aim to break free of the rat race.

Some of you may like to live a life of hedonism and enjoyment within the passive income that exceeds your lifestyle. So be it. Some of you may want rather, to give more of yourself to causes that wouldn't pay well in the real world, for example, volunteer in certain capacities. I realise that with my daughter in my life, I now want to work towards financial freedom because it gives me more time to spend with developing her to the fullest of her potential and to let her grow into the matured, productive and life-changing person that she can be. I also want to be liberated from the rat race to pursue my interests in writing, sharing my own skills and knowledge in areas where I can share and to basically touch lives in ways that I am restricted.

Individuals have told me I can do it WITHIN the rat race by choosing the career that satisfy and to do volunteer work in my spare time. I have tried that out and while I still continue with my career because the earned income helps me accumulate investible savings, I realise the same 24 hours leaves me little time to spend on family and volunteer work while keeping a 9am to 6pm job.

Financial freedom - freedom to do for others as you have done for yourself

Back to our article above. I do believe that it is more blessed to give than to receive. But you still need to take care of yourself and your loved ones first before giving. I have done my share of volunteer work in teaching children reading skills as well as helping out in a supervised homework group program for 5 years or so. I have helped out in a non-profit professional association as a board member that has benefited my peers in the industry in terms of training and experience sharing. I have done for others and it has made me more fulfilled as a person. Now, I realise my focus is on financial freedom so that I can take better care of my loved ones because the time-money trade-off becomes less a burden on me with ever cent that goes into growing my passive income sources.

Would financial freedom make you happy? Why? You may want to take this long weekend to mull about the reasons behind achieving financial freedom. The deeper this desire comes from within, the more the desire is fueled by something more than self-gratification, the more you realise your actions will be aligned to the financial freedom principles:

- Live within your means

- Save and invest

- Grow your means

In the meantime, rest, recreate and refresh yourself over these three days and remember to take care of your health too!

Be well and prosper.

My good friend once remarked that once he had achieved financial freedom, he would want to spend his time drinking a leisurely cup of coffee on weekday mornings and watch the morning crowd pass him by as they go about working for a living.

My good friend once remarked that once he had achieved financial freedom, he would want to spend his time drinking a leisurely cup of coffee on weekday mornings and watch the morning crowd pass him by as they go about working for a living.