How do we invest for financial freedom?

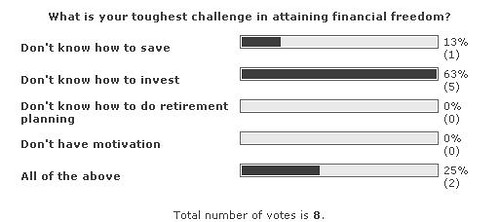

The straw poll that I did yesterday elicited 8 votes and it appears that the majority (63%) felt that "Don't know how to invest" is their toughest challenge in attaining financial freedom. While this poll is not statistically representative since the sample size doesn't even hit 30 for central limit theorem to kick in, it tells me what you would like to know more in our journey together towards financial freedom.

The straw poll that I did yesterday elicited 8 votes and it appears that the majority (63%) felt that "Don't know how to invest" is their toughest challenge in attaining financial freedom. While this poll is not statistically representative since the sample size doesn't even hit 30 for central limit theorem to kick in, it tells me what you would like to know more in our journey together towards financial freedom.

How Panzergrenadier sees investment

For a long time, investments to me was putting money in fixed deposits and savings accounts. My first few years of working while still single and living with my parents was about going to work, earning money, going home, going out during weekends with friends and occasionally dating. The sum total of practical investment knowledge then was put money in fixed deposits. This wasn't a bad strategy then when interest rates were much higher than the paltry 0.25% paid on savings and the 2%+ for fixed deposits that we saw for most of 2007 and likely for the rest of 2008.

Fast forward to 2008 today. Given our low interest rate climate, the only way to grow your money safely in the long term to not only beat the low interest rate but to also beat inflation projected at 5-6% for 2008 is to consider equities (stocks and shares) as well as bonds.

Developing your investment portfolio

If you are serious about developing a portfolio of assets that can beat inflation, then you have to learn about stocks and shares and bonds. I am no expert in this area but fortunately there are many experts out there whose knowledge and know-how can be tapped for free! I highly recommend the following books - "The Intelligent Investor" by Benjamin Graham and "A Random Walk Down Wall Street" by Burton G Malkiel. These are well written books about personal investing and I have read Malkiel's book and have just started on Graham's.

The key take-away from these books is that you cannot beat the stock market consistently as even majority of professional fund managers do not do so year-in-year-out. So the trick is to invest in a portfolio of stocks, bonds and some cash equivalents (treasury bills, deposits) based on your own risk tolerance and do it consistently for next 20-30 years.

I have followed this strategy to some extent in that I now invest in blue-chips for capital gains and dividends. However, I also have deviated by punting on other non-blue chip counters for speculative returns with mixed results.

For me, I have taken a huge swing from my early days of 100% portfolio of investments in fixed deposits and savings deposits to at one stage 90% equities and 10% cash and treasury bills. Going forward, I should move towards an allocation closer to 25-75% equities+bonds and remainder in cash/treasury bills.

Fear of losing money in equities and bonds

If you were like me starting out from a 100% cash/fixed deposits strategy, it's likely that you were also afraid of losing your hard-earned and hard-saved money to the fluctuations in the market. That is perfectly understandable. In fact, many investment books tell you that the first rule of investing is NOT TO LOSE MONEY. Unfortunately, capital preservation is just one consideration, we should then apply our money in investments that grow faster than inflation because if we do not, then we are LOSING MONEY to a lower purchasing power of our savings.

To invest is to make your money work hard for you accordance to your risk tolerance. To do so successfully means you need to understand the potential risks-returns from holding stocks and bonds. You need to determine when to buy and how to select stocks and bonds. You also need to understand your own investment strategy and your targetted returns/risk. You also need to determine how much time and effort you can spare to monitor your investments.

All these feed into your decision making for investments.

It is not easy, but it can bring you closer to your goal of financial freedom.

Be well and prosper.

![]()

2 comments:

I have tagged you in my blog. Is that alright?

Btw, do you put high dividend yield stocks like REITS and Shipping trusts as "near cash" instruments or equity?

Hi dsea

Thanks for tagging to my blog! ;-)

I would put equities as equities, i.e. they are not considered cash equivalents.

The reason is because equities are riskier investments whose market value can go UP or DOWN on any given day. When you need cash and have to liquidate your stocks, you could suffer big losses hence I don't consider it cash as there is some liquidity risk, i.e. to cash out, you suffer losses.

I would rather put treasury bills bought using poems which are very safe yet can withdraw as cash by T+1 as cash equivalents. Hence, when I talk about my portfolio allocation, I am looking at up to 25% in cash/cash equivalents i.e. savings account, fixed deposits, treasury bills or maybe money market instruments.

Post a Comment